by

User Not Found

| Jul 02, 2024

Estate taxes are figured using a person’s cumulative taxable estate after reducing the number by the basic exclusion amount (BEA). While the BEA was nearly doubled from previous levels with the 2017 Tax Cuts and Jobs Act (TCJA), the exemption is

expected to be cut in half at the end of 2025 when TCJA sunsets, leaving some estates with a sharp increase in tax liability. That’s why it’s important to act now to avoid this additional liability in the future.

What is the current estate tax threshold?

The Estate Tax is a tax on your right to transfer property at your death. The includible property may consist of cash and securities, real estate, insurance, trusts, annuities, business interests, and other assets.

For 2024, the estate and gift tax exclusion amount or threshold—the amount a taxpayer may transfer without incurring estate or gift taxes—is $13.61 million for individuals and $27.22 million for couples, which means married couples don't have

to pay estate tax if their estate is worth $27.22 million or less.

In and after 2026, the amount could be reduced to around $7 million for individuals and $14 million for married couples adjusted for inflation. Without additional legislative action by Congress, the ability to transfer wealth from one generation to the

next may be reduced.

What can I do now?

To avoid increased taxes after 2026, estates may opt to make large gifts in tax years 2024 and 2025. In 2019, the IRS clarified that “individuals taking advantage of the increased gift tax exclusion amount in effect from 2018 to 2025 will not be

adversely impacted after 2025 when the exclusion amount is scheduled to drop to pre-2018 levels.”

This is an incentive to use the increased exclusion for lifetime gifting prior to 2026, although that should never be the only consideration in an estate plan.

For instance, prior to 2018, Mr. Smith had not made any taxable gifts. However, in 2019, with the BEA set at $11.18 million, Mr. Smith decided to gift $8 million to family members. By utilizing $8 million of the available BEA, Mr. Smith effectively reduced

the gift tax liability to zero. Unfortunately, Mr. Smith passed away in 2026, where the BEA is projected to drop to around $7 million. Despite this lower threshold, Mr. Smith’s estate can still base its estate tax calculation on the higher $8

million BEA that was used in 2019. This strategy ensures that Mr. Smith’s estate owes no estate tax, leveraging the higher BEA from prior years.

Maximizing gifts in 2024 and 2025

To take full advantage of the current exemption limits before they decrease, consider these additional strategies:

- Irrevocable trusts: Setting up irrevocable trusts can also be an effective way to transfer wealth. Trusts can provide for family members while removing assets from your taxable estate.

Example: Placing

$5 million into an irrevocable trust in 2024 for the benefit of your grandchildren can help ensure those assets are not subject to estate tax when the exemption drops. This example is particularly important as the Generation Skipping Transfer

Tax (GSTT) exemption is separate from, and in addition to, your estate and gift exemption. This exemption provides a way to make gifts to individuals that are two or more generations younger than you without incurring 40% GSTT.

- Consider Spousal Lifetime Access Trusts (SLATs): SLATs allow one spouse to transfer assets to a trust benefiting the other spouse (and potentially children), utilizing the current exemption while still providing indirect access to

the trust's assets.

Example: Transferring $10 million to a SLAT for the benefit of your spouse can reduce your taxable estate and still offer financial support to your family.

- Charitable giving: Large charitable donations can reduce your estate size and provide immediate income tax benefits. Consider charitable remainder trusts (CRTs) or charitable lead trusts (CLTs) for more strategic giving.

Example: Donating $3 million to a charitable remainder trust can provide you with income for life and eventually benefit your chosen charity, reducing your taxable estate.

- Review and update your estate plan: Ensure your current estate plan is aligned with your goals and takes the upcoming changes into account. This may include updating wills, trusts, and beneficiary designations.

Please see our 2022 estate and gift tax planning blog post for more strategies.

How are estate taxes figured?

According to the Internal Revenue Service, “The Estate Tax provisions apply a unified rate schedule to a person’s cumulative taxable gifts and taxable estate to arrive at a net tentative tax. Any tax due is determined after applying

a credit based on an applicable exclusion amount. A key component of this exclusion is the basic exclusion amount (BEA). The credit is first applied against the gift tax, as taxable gifts are made. To the extent that any credit remains

at death, it is applied against the estate tax.”

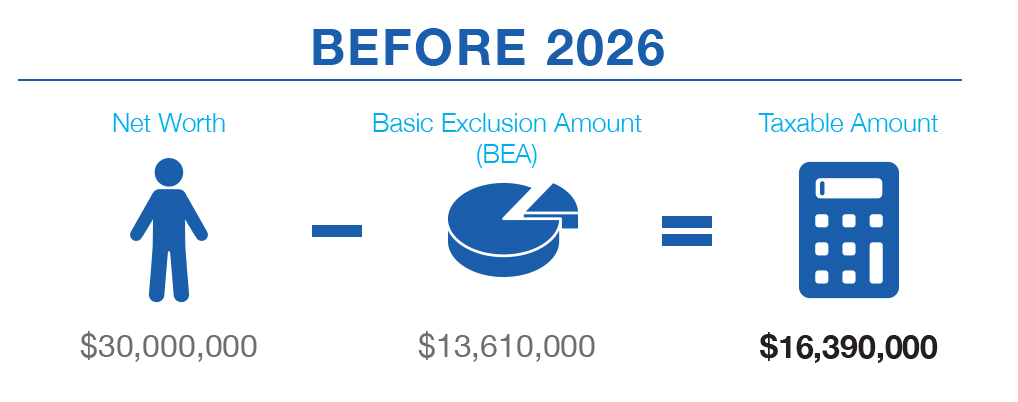

- Current scenario (before 2026):

The current Basic Exclusion Amount (BEA) for estate and gift taxes is $13,610,000 for individuals.

For married couples, the BEA is effectively doubled to $27,220,000 by allowing

the transfer of the deceased spousal unused exclusion (DSUE) amount to the surviving spouse.

If an individual has a net worth of $30 million, we calculate the taxable amount as follows:

• Taxable Amount

= Net Worth - Current BEA

• Taxable Amount = $30,000,000 - $13,610,000 = $16,390,000

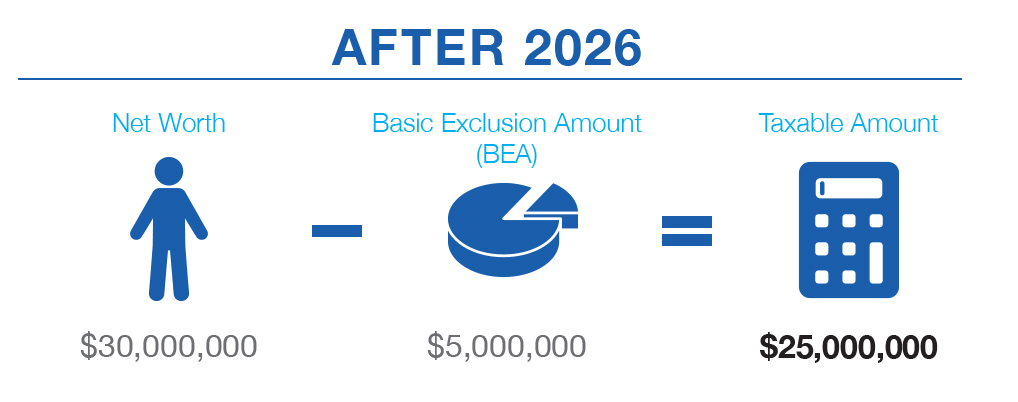

- Comparison with post-2026 scenario:

Starting from January

1, 2026, the BEA will revert to $5 million (adjusted for inflation).

Therefore, if the same individual had a net worth

of $30 million after 2026, the taxable amount would be:

• Taxable Amount (Post-2026) = Net Worth - Post-2026 BEA

• Taxable Amount (Post-2026) = $30,000,000 - $5,000,000 = $25,000,000

With increased estate tax liability on the horizon in 2026, now’s a good time to connect with your financial adviser to discuss options customized to your unique situation. By taking proactive steps now, you can make the most of the current estate

tax laws and secure your legacy for future generations. Get in touch today.

Disclosure: All opinions expressed in this article are for general informational purposes and constitute the judgment of the author(s) as of the date of the report. These opinions are subject to change without notice and are not intended to provide specific advice or recommendations for any individual or on any specific security. The material has been gathered from sources believed to be reliable. However, Badgley Phelps cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. Badgley Phelps does not provide tax, legal, or accounting advice, and nothing contained in these materials should be taken as such.

Originally posted on July 1, 2024